With earnings season underway in earnest this week, we continue to see consumer-facing businesses facing mounting cost pressures from labor shortages and supply-chain constraints. A direct case in point came from Brinker International [EAT], the parent company of the Chili’s and Maggiano chain restaurants, in its recent sharply disappointing earnings pre-announcement. Companies with significant exposure to commodity inputs and labor inputs must raise prices — and if they can’t raise them enough, their margins will suffer. Given that many sectors’ margins have recently been at historic highs, it is not difficult to pencil out a reversion — and that will not be kind to their stocks.

However, consumer-facing companies that have invested heavily in automation, for example, and who have a history of strong supply-chain management will weather this storm. High-quality management remains of utmost importance — which is a further reason why it is important to watch companies consistently over an extended period. If you see a company with excellent management beaten down by a market overreaction, to us, that is a buying opportunity.

With the resolution of the budget wars pushed out to later this year, the market may be waiting to begin pricing in tax increases, which in our view are among the most worrisome prospective market-moving events in the pipeline.

Right now, we are largely focused on commodity suppliers rather than commodity producers; we are particularly interested, as we have said for some time, in tech-related commodities such as rare earths, lithium, and copper. We are also focused on areas that are less immediately exposed to rising input and labor costs — for example, in healthcare (particularly disruptive medical technology, as well as managed care, which we believe will remain the critical delivery component for U.S. healthcare even as it continues to move more towards a government-subsidized and controlled model).

Fintech remains a perennial focus for our interest. Bitcoin has enjoyed another run to new highs — driven perhaps by FOMO (the “fear of missing out”) but also by an increasingly palpable arrival of decentralized cryptocurrencies in the “inflation defense” camp formerly occupied primarily by precious metals. A new futures-based bitcoin ETF reached $1 billion in assets under management within two days — perhaps symbolically eclipsing the 3-day record previously held by GLD. We note that in our view, futures-based products present many technical problems that make them suitable as trading vehicles, but not as instruments to hold long-term. A true bitcoin ETF which holds the underlying has yet to be approved by the SEC. Until then, there is the imperfect but serviceable Grayscale Bitcoin Trust [GBTC], which often trades at a discount to its net asset value, or a variety of reliable and regulated U.S.-based exchanges where consumers can hold bitcoin directly. (For more adept users and long-term “HODLers,” hardware wallets are another option, however with their own risks and challenges.) Bitcoin will likely retreat from its current levels, and we would view such a pullback as an opportunity to accumulate.

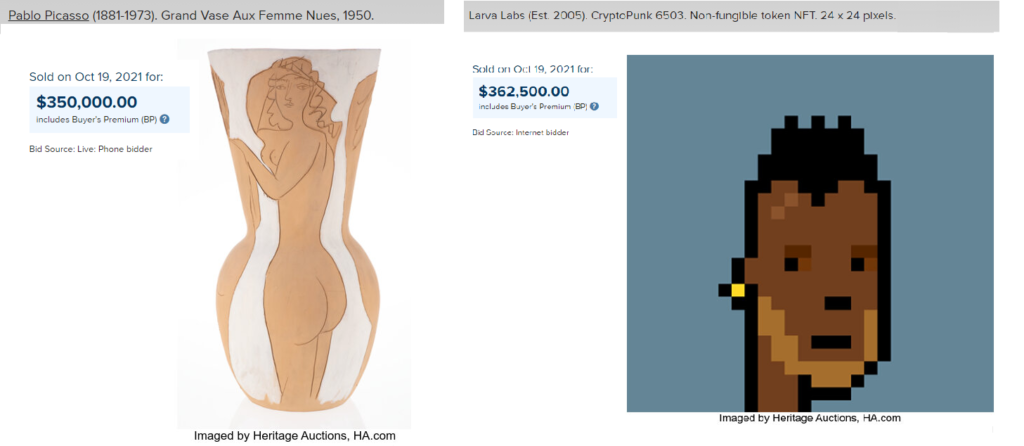

Can’t blame covid for that one. Or can we?

Thanks for listening; we welcome your calls and questions.